News

Investment Markets Update - 3rd Quarter 2025

1st October 2025 Investment Markets Update - 3rd quarter, 2025

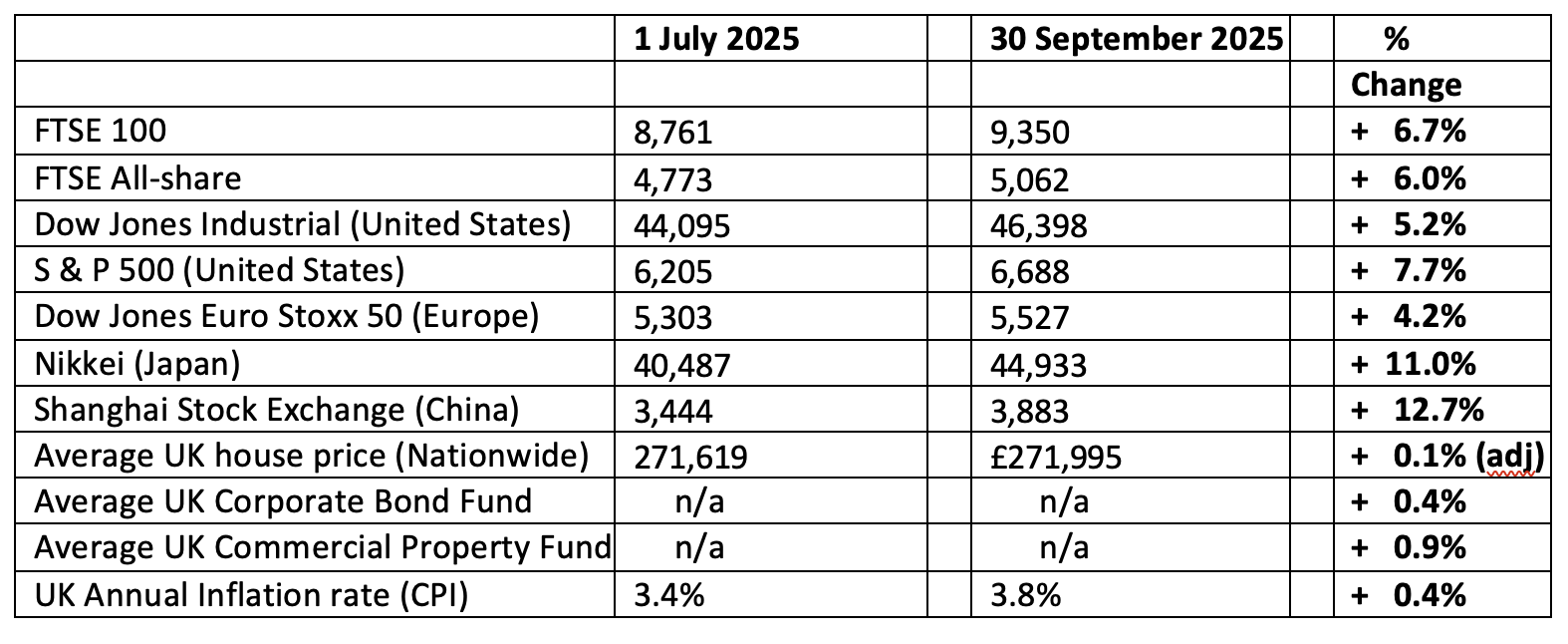

The figures:

The reasons

After the excitement in April, of President Trump's tariffs and subsequent backing off from them, markets have ploughed ahead over the last three months. Technology and AI stocks grew ever higher in valuations, leading some commentators to predict a future crash from these elevated valuations. Expectations of cuts in US interest rates also gave the markets added buoyancy.

The outstanding area to be in was Emerging Markets (with the exception of the Indican markets, which had already seen heady gains) with an overall gain over the quarter of over 12% taking their gains for 2025, to date, to over 30%. This performance followed four years of relative under performance, including a significant fall of almost 20% in 2022. As we have so often pointed out, investments are for the medium-longer term and should be considered as for holding for five years or more. Different sectors move at differing speeds, hence the use of diversification to reduce overall volatility.

The other high performing market was in Japan, where we saw a third quarter gain of +11.0%, as the East outshone its western counterparties. The falling Yen and trade agreement with President Trump after the initial imposition of severe tariffs helped drive Japanese stock values sharply higher.

To the surprise of some, the UK stock markets generally outperformed many others overall, with the FTSE 100 and All-Share indices putting on more than 6% during the Quarter.

The relative laggard equity markets during the summer was in the European sector, with gains of around 4%. The German stock market was particularly poor, although French stocks made a gain of over 3% during the quarter despite the best efforts of their politicians.

Corporate Bonds stabilised after a period of rising yields (thus, falling capital values) and commercial property also continued its relatively positive trend, again after a very difficult couple of years or so. However, Government Bonds look at risk to rising debt in the developed world, and – in the UK especially – inflation proving more “sticky” that had been previously anticipated. I believe that for the UK, inflation is our current largest single risk to the economy and government policy.

Many analysts have pointed to the extremely high valuation rate of the American stock market, in particular the “Magnificent Seven”, primarily consisting of technology companies. The stock price of those companies compared to their annual earnings, has been rising rapidly. This is known as the price/earnings ratio. So typically, in a moderately priced market, you might be expecting a P/E ratio of around 15 times earnings. The US market overall is over 22x. Apple is over 30x Price/Earnings ratio, indicating the markets expects significant growth in that company’s profits in the coming years – but is the potential really there?

By comparison UK stock markets have been trading as low as around 12x P/E over the period, albeit with some increase recently, and a similar story in Japan. Historically, investors buying into markets at the levels of the UK and Japan are typically rewarded over a five-ten year cycle, with often quite significant gains. To me, this looks like a buying opportunity for both of those sectors.

The US market is relying on continued growth of its companies in order to justify the current high level of valuations on their stock prices. If this turns out to be the case, then the stock price is justified and there should be no significant problems. However, in the event of American stocks generally not growing as fast as the market had hoped, there is scope for quite a hard fall. Investors should be aware of this risk, particularly in the shorter term. Looking longer ahead, the US remains the largest economy in the world and is a very entrepreneurial and “go-get” country where capitalism is practiced more completely there, than in any other country worldwide. For these reasons, the US is likely to remain a very good area to invest for the longer term, albeit the prices do currently look high and subject to possible falls in the shorter term.

One asset class that has been outstanding this year is Gold, which has shone more brightly than I can recall. Its value has increased by over 45% so far in 2025. There are a number of reasons for this, including the expectation of lower US interest rates. However, other factors have also come into play. Russia's foreign exchange reserves have been frozen by many countries since 2022 and as a result many Central Banks, including in the emerging markets, have preferred allocations to Gold rather than assets denominated in Western currencies. The unpredictability of the Trump administration has added to this concern. At the same time, the continuing rise in government debt across many Western countries is making Gold appear more attractive than holding large quantities of those currencies.

We have been holding Gold in many of our standard portfolios for some time now, and – alongside technology stocks – this has been our biggest winner over the last couple of years.

Crypto ETNs - now allowed!

As from 8 October, the Financial Conduct Authority (FCA), is allowing “Retail investors” (i.e. Joe Public), to invest in Crypto Exchange Traded Notes (cETNs).

In theory, this means they may be held on platforms, in traditional tax wrappers. How many of the main platforms will allow these investment vehicles to be used remains to be seen, although I'm quite sure that several of the direct-to-customer platforms will be making them available quite quickly.

Essentially an Exchange Traded Note is a promise from the provider to pay a return back to the investor based on an index (in this example, an index of crypto currencies). Unlike Exchange Traded Funds (ETFs), an ETN does not have direct ownership of the assets within that index.

They are listed and traded on exchanges such as the London Stock Exchange, making them accessible through the usual methods.

In the case of UK crypto ETNS, a percentage of the underlying assets must be held as collateral. However, there is no guarantee that this collateral will cover the full value of any holdings - and I expect that they will not - so a major risk is “Counterparty risk”, for example if the issuing provider becomes insolvent, an investor could lose all their money, even if there is collateral in the scheme.

Despite these risks, the Financial Conduct Authority will be allowing retail investors access crypto ETNs, allowing exposure to digital assets such as bitcoins or Ethereum, within standard self-invested pension and ISA accounts.

I am sure that there will be plenty of interest in these products as they become available, but of course, financial advisors everywhere will be making their clients aware of the significant risk and volatility of these asset types. There's a big difference between investing a small amount of money for fun, to see if you can double it, compared to risking a significant part of your retirement savings in such a volatile investment.

Please note these are the views of Christopher Charles Financial Services Ltd, and are for background information only. They do not constitute advice, nor should action be taken without specific advice, pertaining to individual circumstances.Investments can fall as well as rise in value, and you may not get back as much as you invested, particularly in the short term. E & O E – figures are produced with great care, but no liability whatsoever can be accepted for any errors of information within this document. Past performance is not a guide to the future. Christopher Charles Financial Services Ltd is authorised and regulated by the Financial Conduct Authority.

CCFS Ltd, The Dolls House, Teeton Road, Guilsborough, Northampton, NN6 8RB Phone: 01604 740022

A small team committed to guiding your financial journey

As a small company our clients benefit from a personal service from our experienced team who get to know our clients well.