News

Investment Markets Update - 2nd Quarter 2025

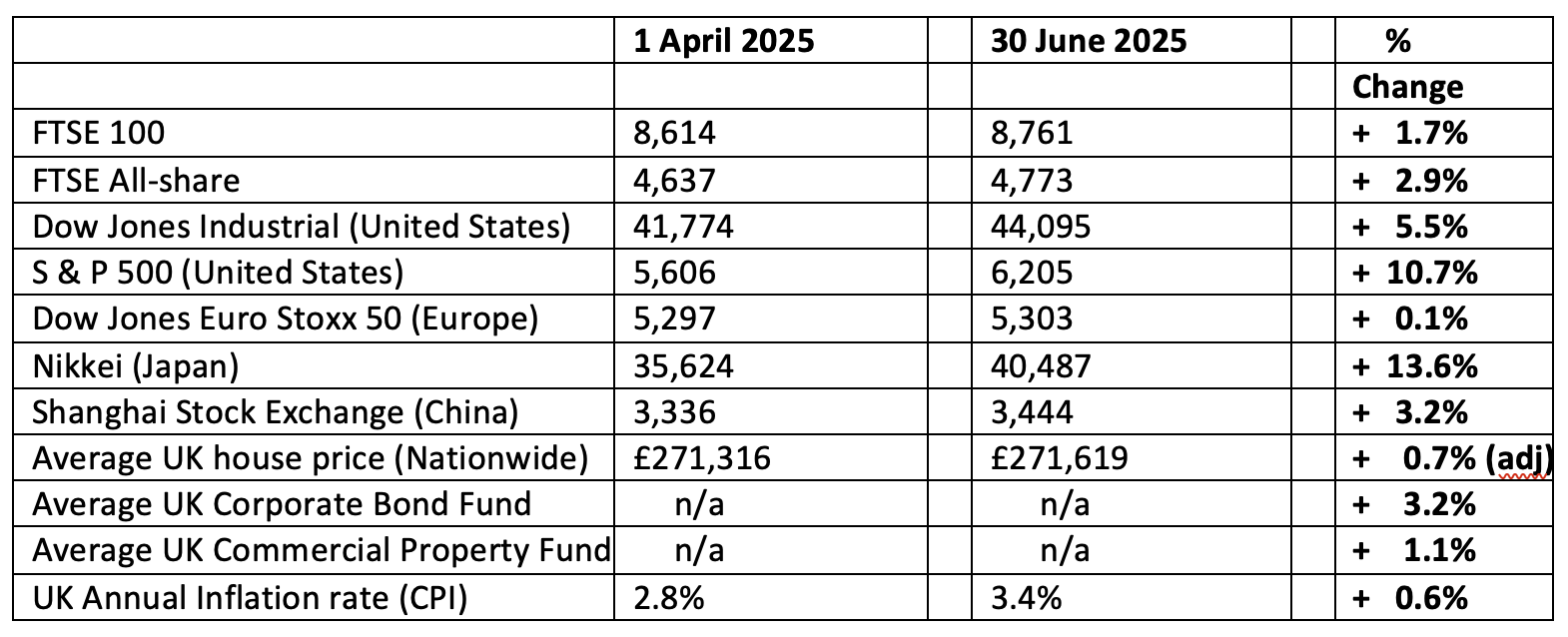

1st July 2025 Investment Markets Update - 2nd quarter, 2025

The figures:

The reasons

Our previous Quarterly update observed that the world was waiting on tenterhooks for “Liberation Day”, which had been slated for 2nd April 2025. This was, of course, President Trump's announcement of tariffs to be imposed on goods entering the United States from abroad. Following an almost surreal presentation on the White House lawns with a scoreboard that would not have been out of place with Eddie Waring’s “It's a Knockout” shows, the markets reacted very badly indeed.

Japan had already seen its main stock market fall by 10% at the end of the previous quarter, and most major stock markets then followed suit, including the US, UK and most European markets. However, the US Bond market reacted equally negatively, causing interest rates on loans to the US government to rapidly increase. Given the enormous size of the US government debt ($37 trillion, or £27 trillion) this would have a significant impact on the finances of the US government, thus forcing President Trump to shortly backtrack on most of his announcements.

Instead, therefore, a “pause” of 90 days was agreed, and also the principles of a trade deal with China - the most important member on the It's-a-Knockout, scoreboard - was agreed, which gave quite significant reassurance to the markets, and heralded the start of the bounce-back.

Subsequently, the rest of the quarter saw developed market equities soaring high, ending with one of the best quarterly figures for some years.

Technology stocks, which had been particularly hard hit with the tariff announcements, benefited in particular from strong earnings announcements, in addition to the pause on tariffs. The “Magnificent Seven” (Apple, Microsoft, Amazon, Alphabet (Google), META (was Facebook), Nvidia and Tesla), between them made a stock price gain of 18.6% over the second quarter. Again, this was a significant outperformance of the remaining 493 companies in the S&P 100 (although technically there are actually 503 companies in the S&P 500).

Bond markets, including all-important US Bonds stabilised, with yields falling back (yields move inversely to prices).

Another emerging theme, despite the recovery in stocks and Bond markets, was the ongoing weakness of the US dollar against other major currencies. In the last three months, the dollar was down around 7% against a basket of developed countries currencies. Ironically, this would have helped US investors who are holding shares in places such as the UK, EU and Asia. Equally, for UK investors, the strong recovery of US shares over the last three months has been somewhat dampened by the fact that the pound sterling has risen against the dollar. The healthy gains of US shares shown in the table above somewhat overstate what the UK investor saw in their pension or ISA or investment account.

If we were to look at the major indices, in their local currencies, then we can see that for the last three months, Asia was the best area to invest in, with Emerging Markets and the US close behind - both regions stock prices growing by more than 10%. After a strong start to 2025, the UK market produced a further steady return in the second quarter, a little ahead of European markets.

Fixed Interest Bonds also saw an improvement over the last quarter, typically in the region of around 3% gains depending on the different markets.

Looking ahead, the markets seem keen to shrug off the risk of further tariffs between the US and other countries. In fact, they appear keen to be shrugging off as many risks as they can, including flash points in the Middle East, slightly stickier than desired inflation levels. Markets continue to anticipate interest rate cuts over the rest of the year and possibly beyond. For the sake of the markets, let us hope that they are correct.

Stablecoins - what are they and will they work?

Readers will be fully aware of the rise and rise of cryptocurrency in the last decade. To the bemusement of many of us in the financial services world, this “currency”, that is not accepted by the vast majority of businesses, continues to gain in value exponentially. This increase in value has continued in 2025, buoyed by the newly elected President Trump, who is keen on this type of asset class.

The detractors of crypto point to the fact that it rarely serves its main purpose, (as a currency) and is merely a speculative bubble just waiting to burst, and maybe it will - though, despite some hefty, short term, falls, it hasn't yet.

The central banks throughout the world have been unable to ignore this new phenomenon, and in attempting to claw back some form of control have been thinking about creating their own versions.

So far, in the United States, we have seen moves towards “stablecoins”. This is essentially a type of cryptocurrency but has the backing of behind a traditional asset such as the US Dollar or possibly gold. The stablecoin market has certainly grown enormously in the last couple of years, with the market dominated by Dollar-backed digital currencies. Already stablecoins are used for more than 6x the amounts of transactions that people use Bitcoin for. However, they are all currently issued only by private companies, and are still subject to risk (such as the Issuer going bust) and volatility, as well as not being legal tender. The US Central Bank does not (as yet) issue stablecoins of its own. This is being considered however, under the idea of the US CBDC (United States Central Bank Digital Currency), sometimes referred to as the Digital Dollar. This would be a form of legal tender, and backed by the US Central Bank.

Meanwhile, the European Central Bank, is likely to adopt a digital currency, the “Digital Euro”, before the end of this decade. This is mainly a more efficient, digital, version of the traditional euro notes. The idea is to reduce the Euro’s dependency on the US payment system but doesn’t create a new currency in any form.

The Bank of England is considering a third option, essentially digital versions of traditional money, known as “tokenised deposits”. These are, essentially, digital representations of commercial bank money, fully backed by real deposits held at a bank (so, not necessarily, the UK’s Central Bank deposits).

The Bank of England Governor, Andrew Bailey, warned recently that privately-issued stablecoins threatened to take “money out of the banking system” and reduce available credit throughout the world. The concern of people like Andrew Bailey and other central bankers is that the spread of stablecoins could undermine those central banks control over money. At the moment, for instance, the control of money in the United Kingdom is heavily managed by the Bank of England, but if a significant number of investors sidestep the traditional form of money, using 3rd party assets such as privately issued stablecoins, then the Bank of England becomes increasingly impotent. The further risk of stablecoins is that the value cannot be guaranteed, against underlying assets such as the dollar, even if the general aim is to do so.

One thing is clear however : money as we know it will be changing rapidly over the next couple of decades.

Please note these are the views of Christopher Charles Financial Services Ltd, and are for background information only. They do not constitute advice, nor should action be taken without specific advice, pertaining to individual circumstances.Investments can fall as well as rise in value, and you may not get back as much as you invested, particularly in the short term. E & O E – figures are produced with great care, but no liability whatsoever can be accepted for any errors of information within this document. Past performance is not a guide to the future. Christopher Charles Financial Services Ltd is authorised and regulated by the Financial Conduct Authority.

CCFS Ltd, The Dolls House, Teeton Road, Guilsborough, Northampton, NN6 8RB Phone: 01604 740022

A small team committed to guiding your financial journey

As a small company our clients benefit from a personal service from our experienced team who get to know our clients well.