News

Investment Markets Update - 2024 as a whole

1st January 2025 Investment Markets Update - 2024 as a whole

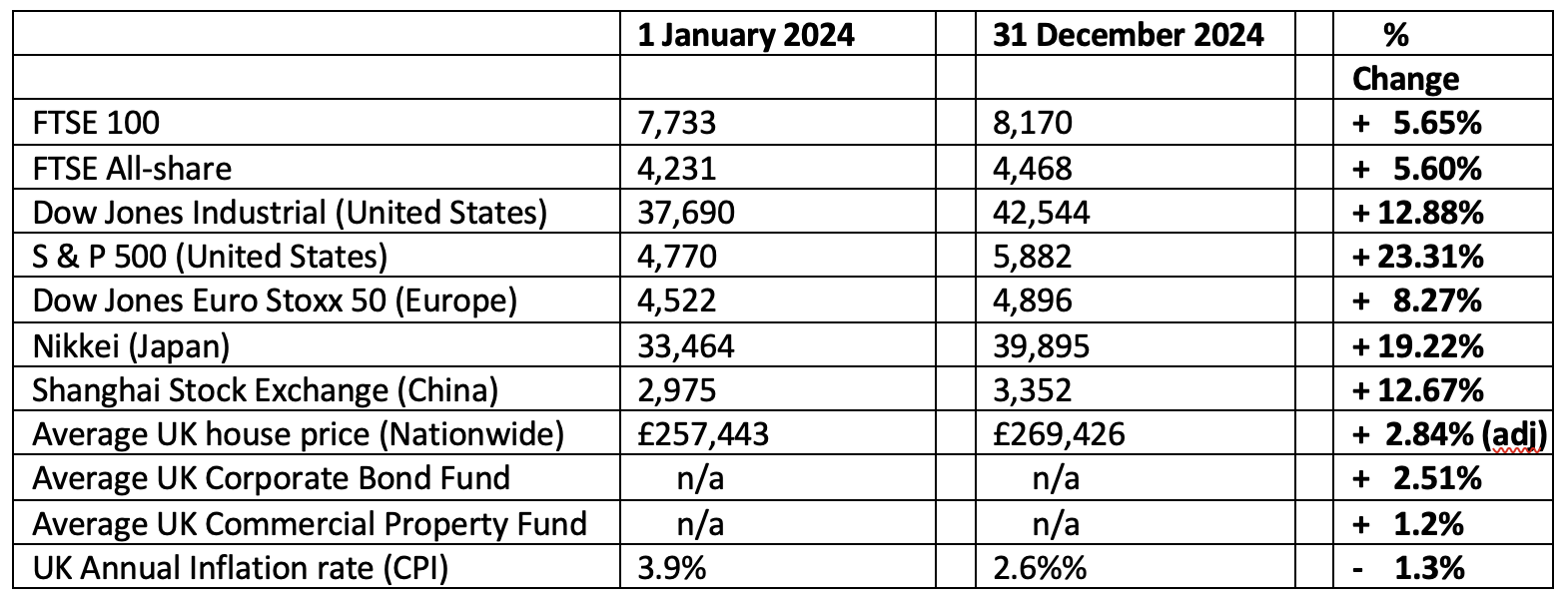

The figures:

The reasons

2024 proved to be a generally positive year for investors, although there were some quite wild differences between asset types and geographical areas in the world.

The standout winner for the year was the United States equity markets. The S&P 500, in particular, made by far the largest gains of any developed markets, assisted significantly by a handful of stocks including the meteoric rise of Nvidia, the technology and AI company, as well as other “magnificent seven” stocks such as Amazon and Apple.

A late rally in the year helped the Chinese stock market produce double digit returns as did Japan also. Emerging Markets such as India, continued to make good progress overall.

One noticeable feature last year was the decoupling of returns in equity markets from the United Kingdom and Europe compared to the much faster growing parts of the world, such as the United States, India and some Emerging Markets. Indeed, as we move into 2025 it is difficult to see how that is not going to continue for the foreseeable future. The risk would be that some of the equity valuations within US stocks in particular are very stretched and we will need to see continued earnings growth within those companies in order to continue to justify the share price. Nevertheless, with the return of President Trump this month, we can expect a deregulated US economy over the next few years, and the markets have reacted favourably to the prospect of a boosting to the economic growth in the US as a result.

During the autumn, the Chinese government also made changes to its economic policies to try to loosen the economy in that area, hence the late rally in the stock market there. There is the hope that 2025 shall see momentum finally regained after the long interruption caused by Covid.

Following a partial recovery late in 2023 and into the start of 2024, Government and Corporate Bonds globally found the going tough during 2024 and, again, as we head into 2025 the markets have raised the yields (interest rate) on Government Bonds in particular due to expectations of higher (“stickier”) inflation than was previously expected. This is, again, influenced by the new incoming US president, who has threatened tariffs on Chinese and European goods. If he follows through with these threats then you can expect higher inflation throughout the world economy in general and therefore, higher interest rates than previously anticipated. This is why we have seen the value of Corporate Bonds fall (Bond prices move inversely to yields).

Nevertheless, there is hope. The Bank of England (and UK financial regulators) have been pressured by the governemnt to target economic growth as well as maintaining financial stability. The UK markets are somewhat torn as to whether we may see as few as two interest rate cuts or as many as six this year. Probably somewhere in between, but if rates do fall (inflation figures permitting) then Bond values can rise again. We have only just started our descent down Table-top mountain, as discussed in our October 2023 update:

Predictions of an extended period of higher interest rates, before a descent proved to be correct

Lower interest rates would be hugely welcomed by the beleaguered commercial property sector, which has been bumping along the bottom for several years now. Changing work patterns continue to make this a difficult-to-read market. In addition, changes to how some of these funds are run are also being made, as FCA pressure to avoid delays in returning capital to small investors during periods of market stress, is being applied to some funds managers of this asset class.

Thinking further about overseas markets, another factor to bear in mind is the strength (or weakness) of the Pound sterling. Last year, it generally fell amongst a range of currencies and in particular against the strong $US. Whilst a weak Pound increases inflation (by making import costs more expensive), it also means UK investors in overseas markets benefit.

As we look to the year ahead, I foresee a continuing movement of investors’ funds away from the UK and Europe and increasingly towards the United States, India and technology stocks in general. If the Pound continues to weaken, as many believe, there’s a further potential benefit there too. Nevertheless, as I have said, US equities, in particular, are expensive and that carries an extra element of risk, hence the usual advice of a diversified portfolio applies, as ever.

Please note these are the views of Christopher Charles Financial Services Ltd, and are for background information only. They do not constitute advice, nor should action be taken without specific advice, pertaining to individual circumstances.Investments can fall as well as rise in value, and you may not get back as much as you invested, particularly in the short term. E & O E – figures are produced with great care, but no liability whatsoever can be accepted for any errors of information within this document. Past performance is not a guide to the future. Christopher Charles Financial Services Ltd is authorised and regulated by the Financial Conduct Authority.

CCFS Ltd, The Dolls House, Teeton Road, Guilsborough, Northampton, NN6 8RB Phone: 01604 740022

A small team committed to guiding your financial journey

As a small company our clients benefit from a personal service from our experienced team who get to know our clients well.