News

Investment Markets Update - 1st Quarter 2025

1st April 2025 Investment Markets Update - 1st quarter, 2025

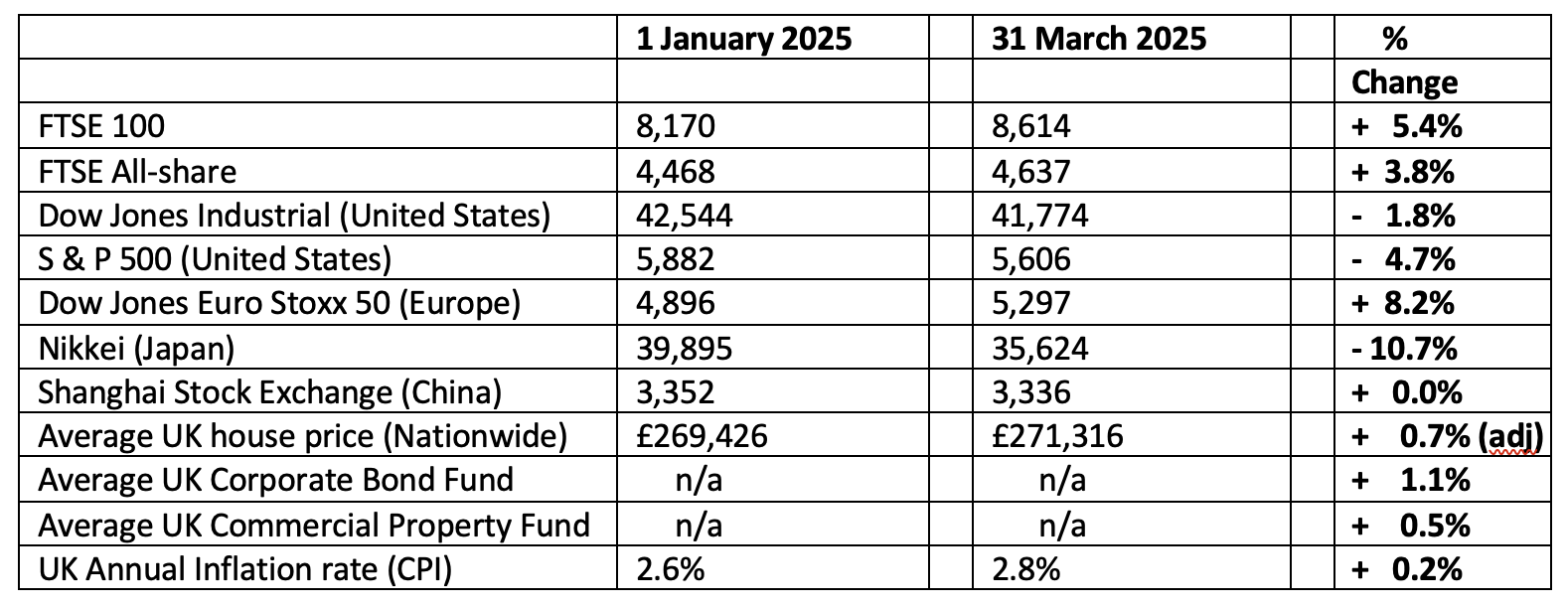

The figures:

The reasons

"When America sneezes, the rest of the world catches a cold."

We have seen a significant turnaround in economic expectations and market sentiment since my investment update three months ago. At that point, US equities had outperformed almost all other regions of the world and was the poster child of the investment world. The thinking was that the new President Trump administration would inject further energy into the economy, with reduced regulatory barriers and an “America First” policy which would create further divergence of economic growth between the US and other major world economies.

However, events have played out somewhat differently than expected with the threat of tariffs making the greatest impact. Already we have seen the US impose significant tariffs on steel imports, which has affected many countries including the United Kingdom whose (already significantly reduced) steel industry looks at risk of complete Death. With President Trump's so-called “Liberation Day” on 2 April, a wide range of further tariffs are anticipated on a wide range of imports to the United States. Inevitably, this will reduce global trade and will push up prices for US consumers. From a UK perspective, there is a risk that stock that can no longer be sent to the US by third countries could be “dumped” into the UK at cheap prices. Whilst this might seem a good thing for consumers, it could risk our own industrial base if we are unable to compete with cheap goods flooding into the UK unexpectedly. In those circumstances, I will anticipate the Government issuing quotas for such imports, rather than bringing in their own tariffs.

There is a real risk that many countries, or the EU as a whole, could retaliate quickly with their own tariffs on imports from the United States, hence lighting the fire for a significant global trade war which could last months or longer.

All of this has led to pessimism over global economic growth in 2025.

Ironically, it has been the US stock markets that have been hit highest over this period with the S&P 500 falling by 4.7%. For UK investors, these falls are compounded by the rise in the Pound sterling, against the US Dollar over the same period. In comparison, Emerging Markets have gained some 3.0% over the first quarter, although there have been large regional differences, with China steady, but India down. Japan has also struggled in the 1st Quarter, hampered by a strong currency and fears of US tariffs. The real winners during this period have been commodities, in particular Gold, which has reached record highs following on from a high return in 2024 as well. As ever, in times of market stress, Gold becomes attractive and rises in value. But remember, it’s a commodity that, in itself, does nothing, creates no jobs and pays no dividends. It’s a volatile asset class and can go down, as well as up.

We have seen some signs of improvement in the Bond and Fixed Interest markets as expectations rise somewhat that interest rates may have to be cut, to stem off potential recessions in the United States, United Kingdom, Europe and elsewhere due to the impending trade tariffs. This is a very tricky situation for the Central Banks to manoeuvre because on one hand they want to avoid recession in their respective regions but at the same time their principal purpose is to maintain low inflation. Tariffs are, in themselves, inflationary and so Central Banks are effectively being asked to “look through” any potential inflation caused by the tariffs and consider them as “one-off” and instead see the bigger picture of potential recession, and cut interest rates accordingly even if the inflation figures do not, in the short term, look as though that would be the normal course of action. Volatility in Bond markets could be set to continue, although we are seeing the benefits of Equity/Bond diversification to a much greater extent than in 2022, when the correlation between the asset classes was significant.

Looking forwards however, it’s all about the “Liberation Day” – 2nd April. At this point, the tariff regime is published, and markets will react accordingly. I expect significant volatility in the days and weeks ahead, whatever the final decisions. The UK government is working hard to avoid tariffs here at home, and of course everyone wants that to work out. However, even if they are successful the UK will still be hit by the rest of the world facing US tariffs, and if other countries do retaliate, we’re in for a rapidly slowing global economy. Again, that old adage still remains true today:

How much Volatility do you want?

“Back in the day”, when I began work in the pensions and investment world, updates to clients’ investments were provided on paper, and sent by post, usually on an annual basis. A good deal of pension funds were invested in “With-profits” funds which were incomprehensible for most clients to understand in any case. But even when the investments were of the more easily understood “Unit-Linked” variety (which we are all used to today) the passage of time over a full year meant that in most cases clients saw an increase in the value of their pension or investment funds.

With the advent of online access people are now able to see their investments literally at the touch of a button. This produces many benefits including the feeling of being closer to your own money and the facility to access it quickly and make investment changes more easily and whenever wanted.

However, I have noted a phenomenon which I am sure is reflected across the country. With the increase of access to the information on their investments and pension funds, some investors find the inevitable movement of markets unsettling. This effect has been compounded by the relatively difficult few years we have endured of late, with COVID, Ukraine and of course the latest round of economic uncertainty caused by the tariffs described above. As with Social Media, there are benefits but also some downsides to the age of information technology.

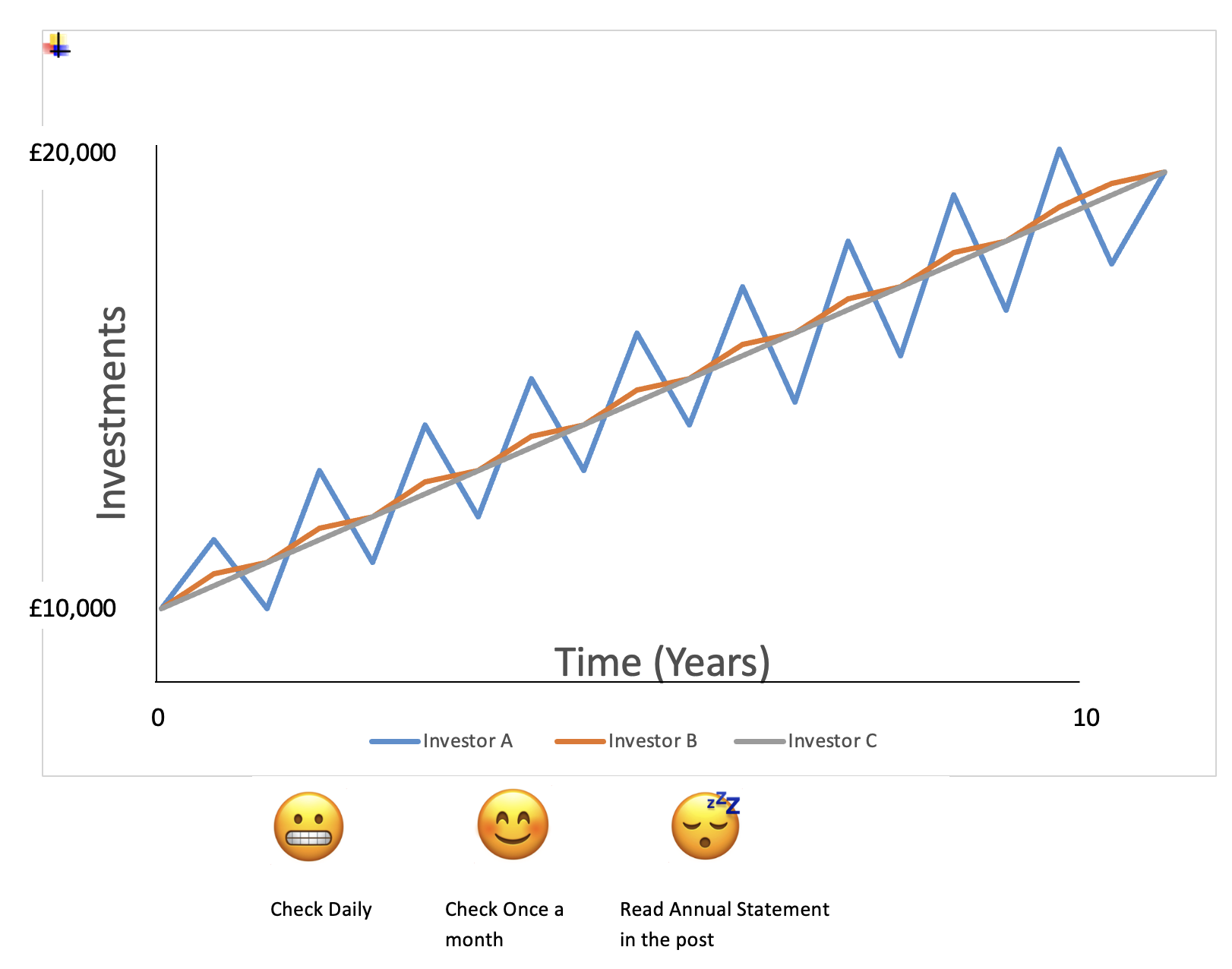

I have therefore shown in the simplified diagram below a way for investors to “reduce” the volatility of their investments, if they so choose. No changes to portfolios need be made. Indeed, nothing need be done at all other than to check one’s investment portfolio less often. As you can see, over a 10 year period the hypothetical £10,000 investment grows to £20,000 (7.2% compound per annum) in all cases. However, the investor checking everyday sees all the fluctuations along the way, which sometimes can be quite severe. The completely laid-back investor checks their statements just annually and perhaps misses opportunities or fails to understand events that may concern them. My example, the happiest and most engaged investor is one who is checking their investments on a monthly basis. In all cases, the investment in my example all end up at the same point in 10 years, but the mental position of the investor may vary considerably along the way.

None of these scenarios take into account investment changes that might be made as a result of more regular checking, hence why I do not usually recommend the “sleepy” investment approach of merely checking on an annual basis. However, there is a happy medium and it often helps to see trends and the bigger picture by checking the progress of one’s investments on, say, a monthly basis rather than too regularly, particularly if a bad day on the stock markets puts the investor in a bad mood for the rest of that day too!

Please note these are the views of Christopher Charles Financial Services Ltd, and are for background information only. They do not constitute advice, nor should action be taken without specific advice, pertaining to individual circumstances.Investments can fall as well as rise in value, and you may not get back as much as you invested, particularly in the short term. E & O E – figures are produced with great care, but no liability whatsoever can be accepted for any errors of information within this document. Past performance is not a guide to the future. Christopher Charles Financial Services Ltd is authorised and regulated by the Financial Conduct Authority.

CCFS Ltd, The Dolls House, Teeton Road, Guilsborough, Northampton, NN6 8RB Phone: 01604 740022

A small team committed to guiding your financial journey

As a small company our clients benefit from a personal service from our experienced team who get to know our clients well.